The Exorbitant Privilege

How America Printed Trillions Without Inflation

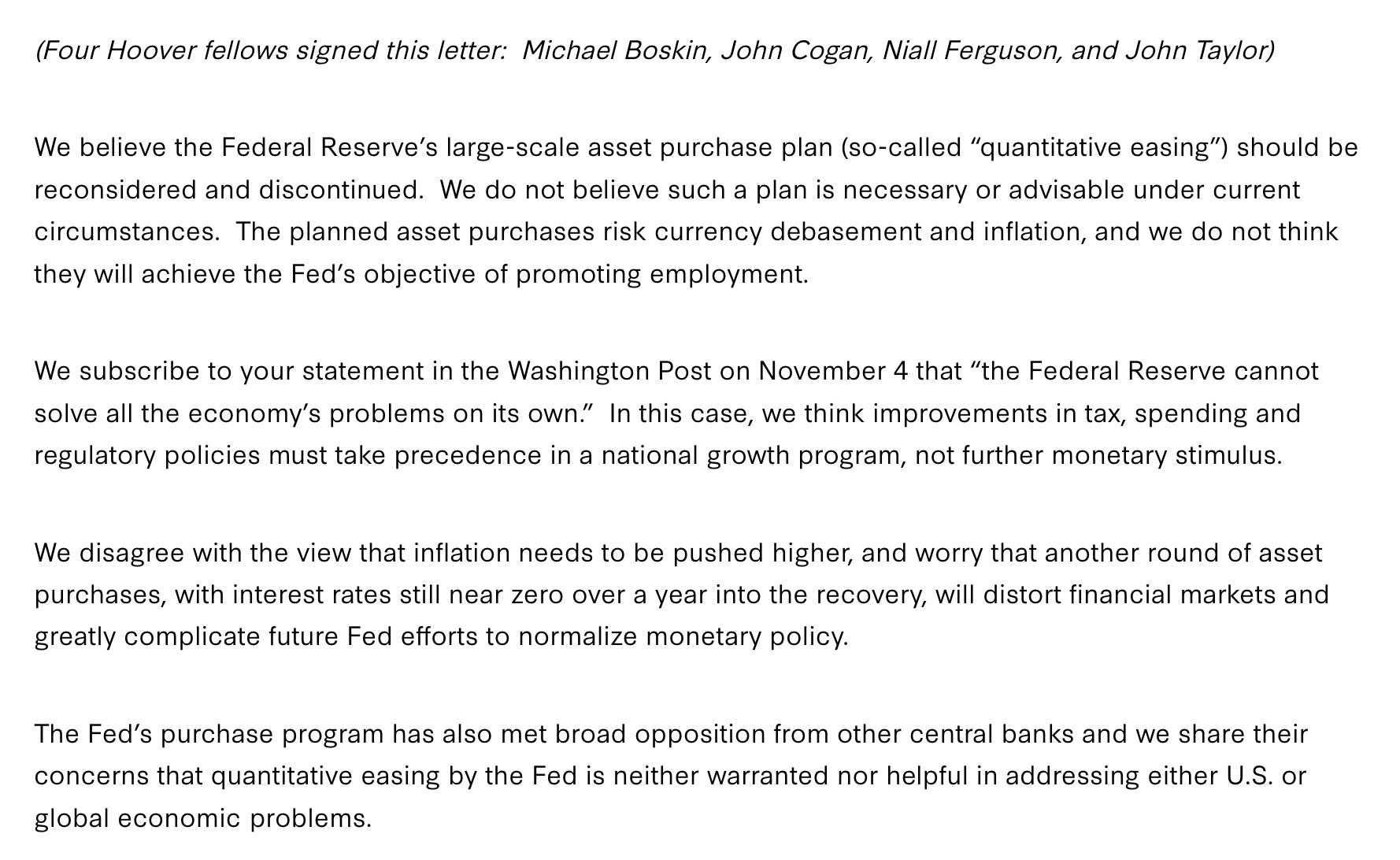

On November 15th, 2010, a group of two dozen economists, investors, and commentators published an open letter to Ben Bernanke, then the Chairman of the Federal Reserve. The Fed had just announced its second round of quantitative easing — six hundred billion dollars of new money to buy Treasury bonds. The letter was short, and its warning was unambiguous. The asset purchases, it read, “risk currency debasement and inflation.” They should be “reconsidered and discontinued.”

In short, these were serious economists and asset managers utilizing one of the tried and true rules of financial history: you print money and prices rise. It is the golden rule that holds from the Roman mint to the Weimar Reichsbank to the central bank of Zimbabwe. Augustus, Diocletian, the Bourbon kings of Spain, the Continental Congress, the Confederacy — every sovereign who ever debased a currency learned the same lesson, usually too late. Create money faster than you create goods, and the money loses value.

There is literally no older or more reliable law in economics.

The signers of that letter were applying two thousand years of evidence. And over the next decade, they were comprehensively, almost embarrassingly, wrong.

The Federal Reserve’s balance sheet went from roughly nine hundred billion dollars in 2008 to four and a half trillion by 2015, paused, and then rocketed to nearly nine trillion by 2022. A tenfold expansion. The largest peacetime money creation in the history of the human species. And for more than a decade, measured consumer inflation sat quietly near two percent — at times the Fed’s problem was that inflation was too low.

The price of bread did not go vertical. The dollar did not collapse. The bond market did not revolt. By every rule that governed Rome and Weimar, it should have.

But it didn’t.

I want to spend the next several thousand words on why — because the answer is not “the old rules are dead.” The answer is far more interesting, and far more useful to anyone managing capital across a long horizon. The old rules were merely deferred. And understanding the mechanism of that deferral tells you exactly where the bill is, who is holding it, and what makes it come due.

The Oldest Trick

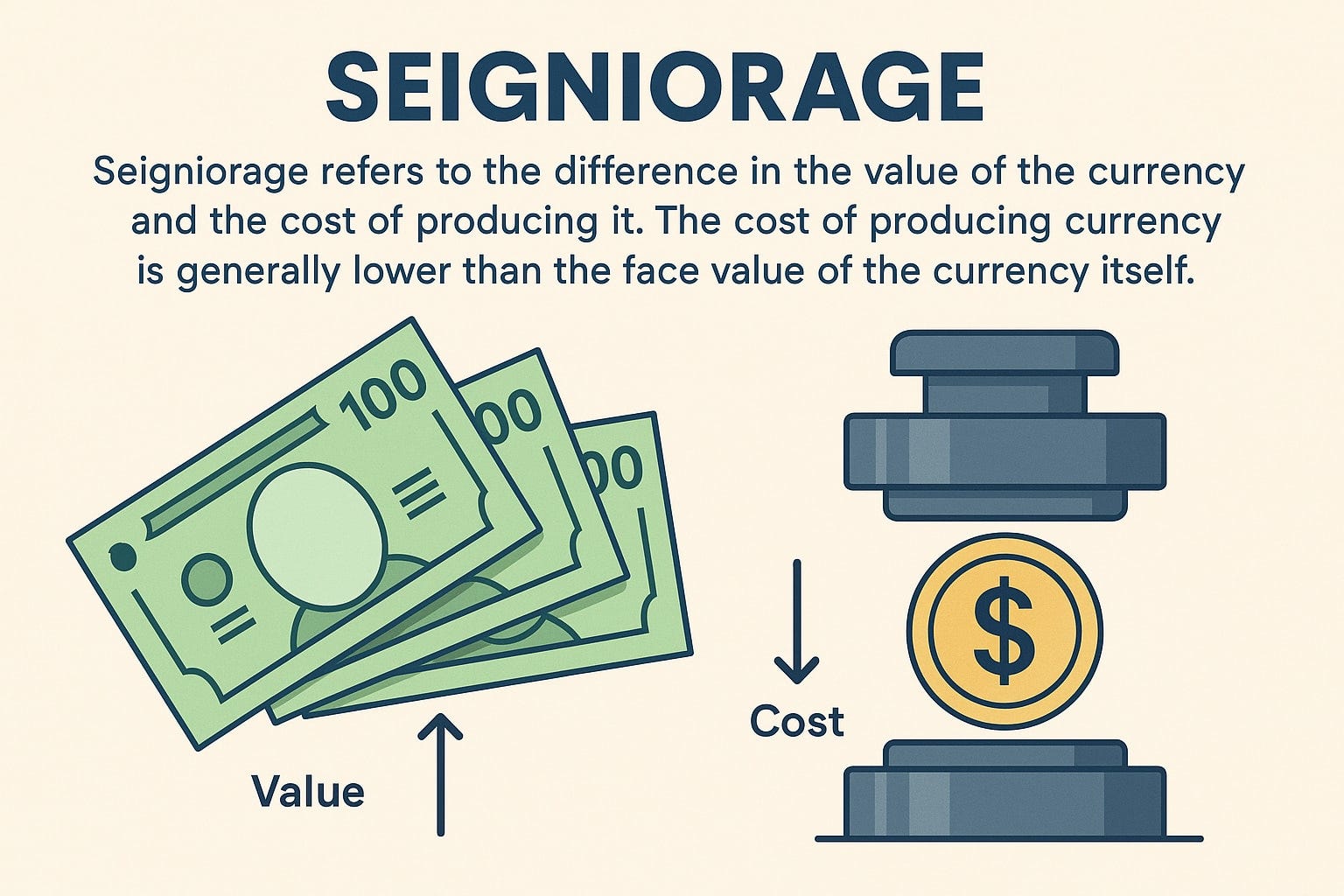

Let’s start with a word - an old word. Seigniorage is the profit a sovereign earns from creating money. The name comes from the French seigneur — the feudal lord who owned the mint and took a cut of every coin struck.

In its oldest form it was physical.

A medieval king would take in silver, mint it into coins, and return slightly less silver than he received — keeping the difference. Later sovereigns got greedier and more clever: they reduced the silver content of the coin while keeping its face value the same. The Roman denarius was about 95 percent silver under Augustus. By the third century, its successor coin was less than 5 percent silver — a copper slug with a thin wash that wore off in your hand. The emperors had discovered they could mint more coins from the same silver, and spend the difference on legions and bread.

That is seigniorage.

And here is the crucial point: it is a tax. A hidden one. When the sovereign creates new money and spends it, that money competes with the money already in your pocket for the same goods. Your money buys less. The purchasing power that leaves your wallet has been quietly transferred to whoever spent the new money first. No vote, no statute, no collection agency. Just a slow, silent transfer from savers to the sovereign.

It is the most politically seductive tax ever invented, because no one can see the taxing authority. Prices simply “go up,” and the public blames merchants, speculators, foreigners, and greed — anyone but the mint. Diocletian, facing the inflation his own predecessors’ debasement had caused, issued the Edict on Maximum Prices in 301 AD and threatened to execute merchants for charging what the market demanded. He blamed “avarice.” He never once mentioned the coin.

Now scale that mechanism up to a country that issues the currency the entire world is built on, and you begin to see the size of what America is actually running.

The American Machine

Now - the concept is pretty easy to understand when we talk about “silver coins” and literally taking silver out of the coin. How, you might ask, does this actually work when we produce paper money?

The United States earns seigniorage three ways, and they stack.

The first is the literal mint. It costs the Bureau of Engraving and Printing a few cents to print a hundred-dollar bill. The difference between that cost and the hundred dollars of goods it commands is seigniorage in its purest, oldest form. Small, but real.

The second is the modern, financial version, and it is larger. When the Federal Reserve does quantitative easing, it does not print paper. It creates bank reserves with a keystroke — money that did not exist a moment before — and uses them to buy interest-bearing assets, mostly Treasury bonds and mortgage securities. The Fed then collects the interest on trillions of dollars of bonds it acquired at zero cost of production. After expenses, it remits the profit directly to the Treasury. In the peak QE years, that remittance ran over a hundred billion dollars annually. The government, in effect, was paying interest to itself and pocketing it. That is seigniorage in a different form.

The third is the one that matters, and it is the reason this essay exists. The United States issues the world’s reserve currency. Foreign central banks hold trillions in dollar reserves. Roughly half of all international trade is invoiced in dollars. And an estimated trillion dollars or more in physical hundred-dollar bills circulates outside the United States entirely — under mattresses in Buenos Aires, in safes in Lagos, in cash economies on every continent. Every one of those bills is an interest-free loan from a foreigner to the United States. They gave up real goods to obtain that paper, and the paper sits there, costing America nothing.

In the 1960s, the French finance minister — later president — Valéry Giscard d’Estaing gave this a name that has never been improved upon. He called it America’s exorbitant privilege. France resented it then and resents it now, because the privilege is real: the United States extracts seigniorage not merely from its own citizens, as Rome did, but from the entire world that uses its money.

The deepest form of tribute in the modern world is not gold carried to a capital. It is the willingness of foreigners to hold your paper for free, indefinitely, and ask for nothing but more of it.

Hold that idea, because it is the hinge of everything that follows. The reason America could print trillions without inflation is the same reason it is an empire. And the reason the privilege might end is the same reason every empire before it declined.

The Puzzle Then

So here’s the thing. The money supply did explode. That part of the warning was correct. So why didn’t prices?

The answer is that the relationship between “money” and “prices” runs through two variables: where the money goes, and how fast it moves. The quantity of money is only the beginning of the story. Newly created money does not raise the price of bread unless it actually reaches someone who is going to buy bread. If it sits idle, or gets absorbed by someone who has no intention of spending it on goods, then the link between money and consumer prices simply breaks.

Between 2008 and 2020, that link broke in five distinct ways at once. Take them in order.

One: the world is a sink for dollars. This is the privilege in action. When you are the reserve currency, global demand for your money is structural, enormous, and growing. Newly created dollars get absorbed into foreign reserves, trade settlement, and offshore savings rather than bidding up American goods. America can do something no other nation can: it can export its inflation. Rome could not ship its debased denarii to another nation. The dollar flows out and simply… stays out. The pressure that would have shown up as domestic inflation is dissipated across the entire globe.

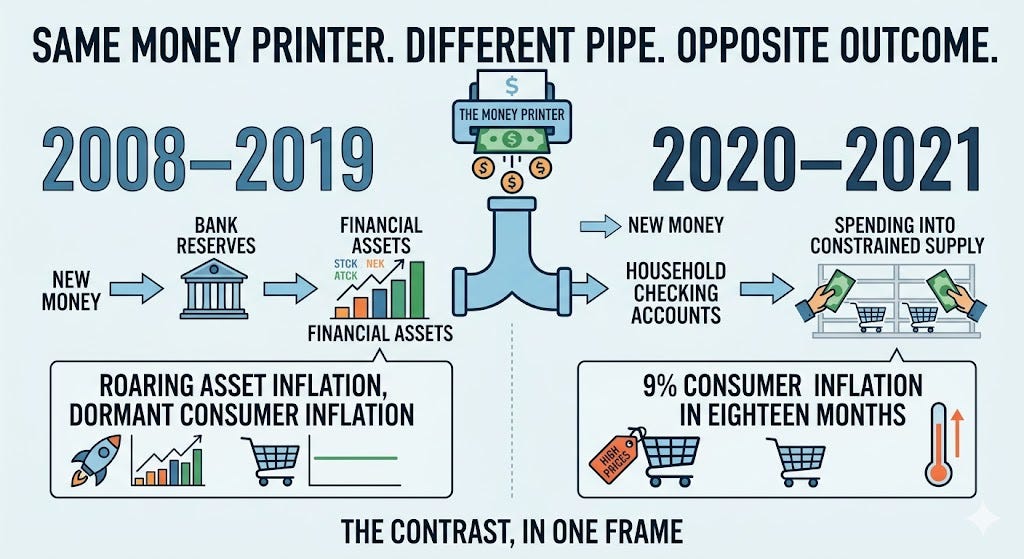

Two: QE created bank reserves, not spending money. When the Fed bought bonds, it credited the selling banks with reserves. But those reserves did not become loans, and loans are how money actually enters the real economy. Critically, in October 2008 the Fed began paying interest on reserves — so banks had every reason to park the new money right back at the Fed and collect a risk-free yield rather than lend it out. The monetary base exploded. Broad money — the money you and I actually spend — grew at a fraction of that rate. The trillions never reached the bread aisle because they never left the financial plumbing.

Three: velocity collapsed. There is an old calculation in economics: money times the speed at which it changes hands equals prices times output. M times V equals P times Q. The warning letters all focused on M. They forgot V. And in a deleveraging economy — households paying down debt, banks hoarding capital, firms wary of investing — the velocity of money fell off a cliff. A dollar that used to change hands a dozen times a year now sat still. Rising M was met by falling V, and the two roughly cancelled. Money that does not move simply does not move prices.

Four — the Cantillon effect. New money is never neutral. It enters the economy at a specific point and enriches whoever touches it first, before prices adjust. The eighteenth-century banker Richard Cantillon worked this out three hundred years ago. Post-2008 money entered through the financial system — so it inflated financial and hard assets: bonds first, then equities, then real estate. We did not avoid inflation. We had ferocious inflation. It simply showed up in the S&P 500, in the price of a first home, in farmland and fine art — none of which sit in the Consumer Price Index. “There was no inflation” is what comfortable people say. Ask anyone under forty trying to buy a house whether the last fifteen years felt like price stability. The money went somewhere. It went to people who already owned assets. That is not a side effect of QE. That is the mechanism of QE.

Five: powerful disinflation was running underneath the whole time. Chinese manufacturing and global supply chains were pushing goods prices down for two decades. Technology was relentlessly deflationary. Aging demographics suppressed demand. A mountain of private debt smothered velocity further. The Fed was pressing the accelerator, but the structural road was sloped steeply downhill in the other direction. For a decade, the two forces met near zero, and we called the result “two percent inflation” as though it were a triumph of policy rather than a coincidence of opposing pressures.

Five mechanisms with one inevitable conclusion. The thing that dictates the ultimate inflation level is less about the quantity of money, but rather the channel through which the money flowed.

The Tell

If that thesis is right, it makes a prediction. Change the channel — get the money out of the financial plumbing and into the hands of people who will spend it on goods — and you should get consumer inflation, fast, even in the same country with the same central bank.

In 2020, we ran exactly that experiment.

The pandemic response did not look like 2008. It was not QE quietly swelling bank reserves. The government wired money directly to households: stimulus checks deposited into tens of millions of checking accounts, expanded unemployment benefits that in many cases exceeded prior wages, forgivable PPP loans to businesses. This was not money parked at the Fed. This was helicopter money, and it landed in the hands of people who immediately spent it — into an economy whose supply chains were simultaneously seized up.

And guess what? The result arrived on schedule. Consumer inflation tore to roughly nine percent by the middle of 2022 — the highest reading in forty years. The bond market repriced violently. The Fed hiked interest rates at the fastest pace in a generation.

This is the tell. This is the natural experiment that confirms the entire mechanism. The same nation, the same currency, the same central bank, produced two opposite outcomes from two different transmission channels.

It is not how much money you print. It is whether it reaches a spender — and whether the world is still willing to absorb whatever spills over.

Why Rome and Weimar Were Different

Return now to the signers of that 2010 letter, armed with the mechanism, and you can see precisely why their two thousand years of evidence misfired. Every historical debasement they had in mind shared three features the post-2008 United States did not.

The debased money was spent directly into circulation. When Rome clipped the denarius, it spent the new coins immediately — on soldiers, on the grain dole, on public games. The money went straight to people who spent it on goods. There was no financial system to absorb it into idle reserves; there was no S&P 500 to soak it up. Roman wheat prices rose roughly two-hundred-fold from the first century to the fourth. The channel was direct, so the inflation was direct.

There was no external demand to absorb the excess. No foreign central bank wanted to hold the third-century denarius as a reserve asset. No one in Gaul was stuffing debased Roman coins under the mattress as a store of value. The currency had nowhere to go but into domestic prices. America’s escape valve — a planet that wants its money — simply did not exist for any prior debaser.

Confidence broke. This is the accelerant. In Weimar Germany between 1921 and 1923, the truly fatal moment was not the printing itself but the day the public understood it. Once Germans grasped that the mark would be worth less tomorrow, they spent it instantly — velocity didn’t collapse, it went vertical, the exact opposite of post-2008 America. Money became a hot potato. Prices doubled in days. Hyperinflation is not fundamentally a monetary event; it is a psychological one. It is what happens when a population loses faith in the currency all at once.

Zimbabwe, Venezuela, the Confederacy, the French assignats — run the checklist and they all rhyme. Money spent directly into circulation. No external sink. Collapsing confidence, often atop collapsing productive capacity.

The post-2008 United States defused all three. The money went into reserves and assets, not the grocery store. The world stood ready to absorb the overflow. And confidence in the dollar — far from breaking — strengthened, because in every crisis of the period, frightened global capital ran toward the dollar, not away from it. The privilege fed on itself.

For now.

The Timeless Turn

Now, listen, the comfortable version of this essay ends at section six. “America is special, the rules don’t apply, hold equities, relax.” That is the story the last fifteen years has trained everyone to believe, and it is precisely the story that should worry you.

Readers of this letter will recognize the framework from The Stages of Imperial Decline. The reserve-currency privilege is Stage Two — currency debasement and financial engineering — operating with a structural escape valve that no prior empire possessed. That escape valve is real. It has held for eighty years. And the cardinal error of the bull case is to mistake a temporary exception for a permanent law of nature.

Remember what reserve status actually is. It is not a gift, and it is not an entitlement. It is a consequence of imperial strength — military, economic, institutional, and most of all credible. Sterling was the world’s reserve currency for roughly a hundred and twenty years. The British believed it was simply the natural order of things. Then the math stopped working, and in November 1956 the United States Treasury sold sterling on the open market to break the pound, and Britain folded a war in forty-eight hours. The reserve privilege did not protect the empire. The empire was what had created the privilege, and when the empire weakened, the privilege evaporated with it.

And the privilege is being tested, right now, at the margins, in ways that would have been unthinkable a generation ago:

In 2022, the United States and its allies froze the dollar reserves of the Russian central bank. The intent was to punish an aggressor. The lesson absorbed in Beijing, Riyadh, Delhi, and every non-aligned capital was simpler and more durable: dollar reserves are only yours until Washington decides otherwise. That is the sort of hard realization that is hard to unlearn.

Central banks have been buying gold at the fastest pace in modern record — a quiet, collective hedge against the very paper they are supposed to hold.

De-dollarization is mostly noise today, and I will not pretend the renminbi is a serious reserve alternative — it is not, not with capital controls. But the direction of travel matters more than the current level.

And underneath it all sits a fiscal trajectory that erodes confidence by the year: federal debt held by the public above 100 percent of GDP, a peacetime deficit over six percent of GDP at full employment, and net interest on the debt now exceeding the entire defense budget.

Here is the key insight, the one I most want you to carry out of this essay. The absence of inflation was never proof, per se, that we have an endless free lunch. It was, ultimately, the world carrying America’s inflation bill by holding its paper. Every dollar held abroad, every Treasury stacked in a foreign reserve account, every hundred-dollar bill in a Buenos Aires safe is a deferral of the inflation that the textbook said should have happened. The privilege and the vulnerability are not two things. They are the same fact, viewed from opposite sides. The day the world’s willingness to hold dollars thins — the day the sink stops absorbing — the inflation that was exported for forty years begins, at the margin, to come home.

I am not predicting that day. I do not know its date, and neither does anyone selling you a date. The base rate for great powers escaping this pattern is not encouraging, but Britain proved a managed, graceful decline is at least possible. The point is not to predict the year. The point is to understand the structure, so that you are positioned correctly whenever it arrives.

Positioning — The Operator’s Read

This is the part that separates this letter from commentary, so let me be concrete. If seigniorage is a tax on holders of money, and if the reserve privilege is a real but finite deferral of that tax, then the implications for a serious allocator are not ambiguous.